For years, the advice around the Portland metro was almost automatic. If we wanted access to Portland but hoped to protect income, we went north. Live in Vancouver. Work wherever we wanted. Enjoy Washington’s lack of state income tax.

That was the playbook.

Now the playbook is changing, and not in some small technical way. Washington has passed major new tax legislation, expanded its tax framework, and chipped away at the very advantage that made the Washington side of the river so appealing for retirees, high earners, and relocation buyers.

At the same time, the old real estate argument has weakened too. The idea that we cross the river and get dramatically more house for less money is no longer the clean, obvious truth it once was.

If we are deciding between Oregon and Washington today, especially around Portland and Vancouver, we need a more current analysis. Not old advice. Not slogans. Actual numbers.

Table of Contents

- Why Washington Used to Be the Obvious Choice

- The Value Gap in Housing Has Narrowed

- Washington’s Tax Advantage Is No Longer as Simple

- The Costs People Forget About

- Oregon’s Sales Tax Advantage Is Bigger Than Most People Realize

- What Migration Trends Are Really Telling Us

- Where Oregon Is Still More Expensive

- A Real-World Cost Comparison

- Why Many People Still Choose Oregon

- Final Thought

- FAQ

Why Washington Used to Be the Obvious Choice

Oregon has long had a significant state income tax. The top marginal rate is 9.9%, which puts it among the higher income-tax states in the country.

That mattered a lot for people moving into the Portland area. If we could live 20 minutes away across the river in Clark County and still access Portland jobs, Portland amenities, and Portland family, the math often pointed north.

For a retired couple bringing in $200,000 a year from IRA distributions and investment income, the difference could be huge. It was entirely realistic to see annual savings in the range of $15,000 to $20,000 per year by living in Washington instead of Oregon.

Over a 10-year retirement, that could add up to $150,000 to $200,000. That is not a rounding error. That is travel, gifting, flexibility, and legacy.

For decades, that was a compelling case. Many families made exactly that move for exactly that reason. It was rational then.

The Value Gap in Housing Has Narrowed

The second leg of Washington’s old advantage was housing. We used to be able to say, with a straight face, that Vancouver and much of Clark County offered more home for the money.

Bigger lots. Larger houses. Newer construction. Lower prices.

That gap has narrowed dramatically, and in some areas it has reversed.

Using the numbers highlighted here for 2026, the average home price in the Vancouver, Camas, and Washougal area sits at approximately $628,000. Portland sits at approximately $609,000.

That means the old “cross the river for better value” story is no longer broadly true at the market level. In fact, the premium to live in Vancouver over Portland, based on those averages, is about $19,000.

Now, we always have to be careful with averages. Real estate is hyper-local. There are absolutely pockets of Clark County with value. There are also Portland neighborhoods that are far more expensive than anything in Vancouver.

But the broader narrative matters because it shapes decision-making. And the broader narrative has changed.

Even local reporting in Clark County has pointed to the same issue. Housing affordability there is slipping relative to the old expectation. Supply and demand have tightened. Prices have risen. In many neighborhoods, buyers are no longer getting the dramatic bargain they once expected.

So if the old Washington value proposition was built on two legs, no income tax and more house for the money, both legs are weaker now.

Washington’s Tax Advantage Is No Longer as Simple

This is where the conversation gets much more important.

Washington already passed a 7% capital gains tax on capital gains over $250,000, and that tax has been upheld and is currently being collected. That matters because it was the first real crack in the “no income tax” identity that defined Washington for so long.

Then came the 2025 tax package, described as the largest in Washington state history. That package included:

- Significant gas tax increases

- Continuation and enforcement of the capital gains tax

- Fee increases

- Legislative language that creates a framework for a broader state income tax structure

That last point is the one many people will want to pay attention to.

The issue is not only what Washington taxes today. It is where the state appears to be heading. For anyone making a 20-year retirement decision or a long-term relocation decision, trajectory matters almost as much as the current line item.

The legal and political environment has shifted. What once felt impossible now has a framework. That means we should not analyze Washington based only on yesterday’s reputation.

This is not a prediction that a broad income tax is definitely arriving tomorrow. It is a reminder that the architecture is being built, and long-term planning should account for that risk.

The Costs People Forget About

When people compare Oregon and Washington, they usually get stuck on one line item: state income tax.

That is a mistake.

There are several other costs that quietly reshape the equation.

1. Washington’s real estate excise tax

Washington charges a real estate excise tax, often called REET, every time a property is sold. It is paid by the seller, and it is not small.

On a home sale between roughly $525,000 and $1.5 million, the average rate discussed here is around 1.28%. On a $1 million home, that is about $12,800.

At $1.5 million, the next bracket begins to apply and the cost can climb much faster.

Oregon does not have a comparable statewide real estate excise tax. For many families, that means a future sale in Oregon preserves more equity for retirement, downsizing, or heirs.

It is easy to dismiss this because it does not hit on purchase day. But homes eventually get sold. Whether that happens in 10 years, 20 years, or through estate settlement, that tax is part of the long-term cost of ownership in Washington.

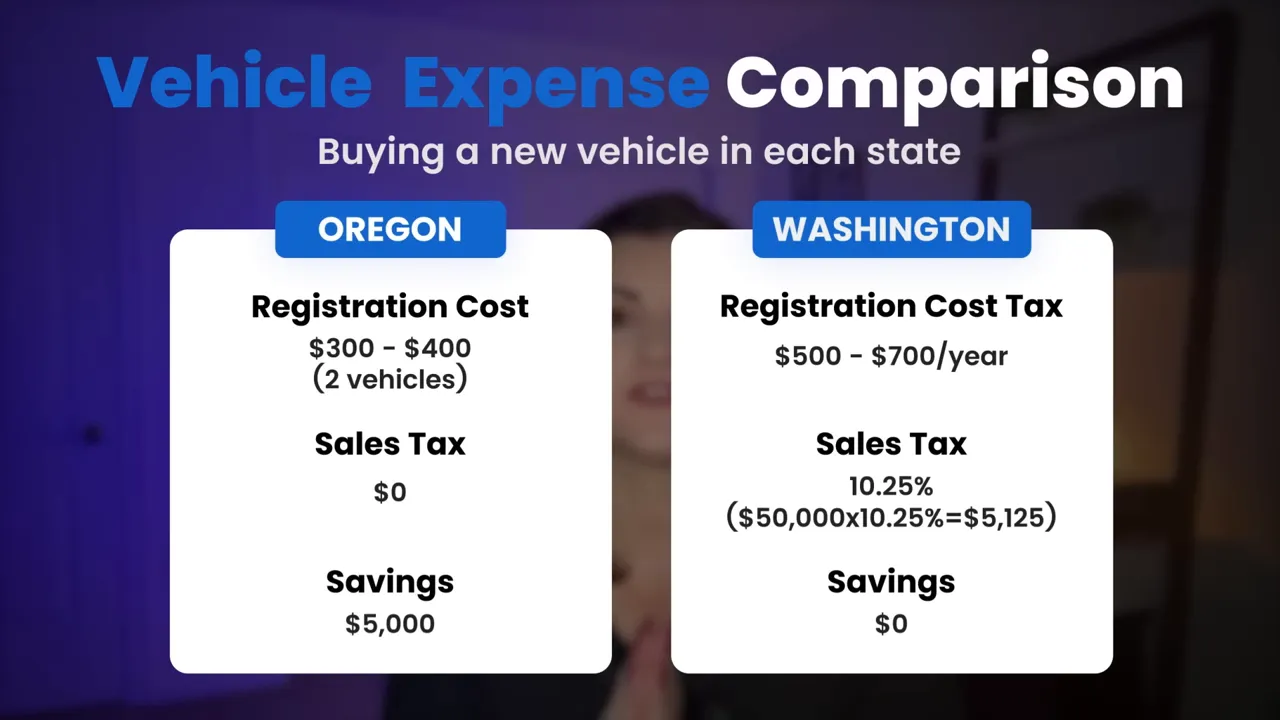

2. Vehicle registration costs

Vehicle expenses are another overlooked category.

In Washington, especially in areas affected by transit-related fees, vehicle registration can be much more expensive than people expect. The examples here estimate registration for two vehicles at roughly $1,400 to $1,800 per year.

In Oregon, that same rough comparison comes in closer to $400 per year.

That is not going to outweigh income tax by itself, but over a decade it adds up.

3. Sales tax on vehicle purchases

This one gets very real, very fast.

Washington’s sales tax in many areas runs around 10.25%. On a $50,000 vehicle, that is about $5,125 in sales tax the moment we buy it.

Oregon has no sales tax.

So when we buy a car in Oregon rather than Washington, the day-one difference can easily be around $5,000 on that one purchase.

Oregon’s Sales Tax Advantage Is Bigger Than Most People Realize

This is one of Oregon’s most underappreciated financial advantages.

Not low sales tax. No sales tax.

Washington’s sales tax generally falls between 9% and 10.5%, depending on location. Clark County is in that range.

That affects far more than big-ticket items. It touches daily life.

Dinner out. Household purchases. Furniture. Electronics. Gifts. Home goods. Everything we spend throughout the year starts carrying a silent premium in Washington.

Using the example here, if a household spends $80,000 to $100,000 annually, that could mean a savings of roughly $7,000 to $10,000 per year by living and spending in Oregon instead of Washington.

That is the part many people miss. Oregon’s high income tax is obvious. Oregon’s no-sales-tax advantage is quieter, but for many households it is substantial.

As Washington’s tax environment becomes more layered, Oregon’s sales tax advantage gets more valuable, not less.

What Migration Trends Are Really Telling Us

There has been a lot of noise around people leaving Oregon, but that headline often leaves out the real story.

Multnomah County has seen population decline. That part is true.

But Washington County and Clackamas County have gained residents in that same general window. Add counties like Marion and Deschutes, and the picture gets a lot more nuanced.

What this suggests is not a simple Oregon exodus. It suggests an internal reshuffling.

Many people are not leaving the region entirely. They are moving out of Portland proper and into suburban areas that offer more space, more stability, and in some cases a more manageable tax picture than Multnomah County.

That shift matters if we are thinking about where demand is strongest in the Portland metro. It also matters if we have been assuming that Portland-area growth is dead. It is not. The center of gravity has simply shifted.

Places like West Linn, Sherwood, Beaverton, and other suburban pockets continue to draw attention for exactly that reason.

Where Oregon Is Still More Expensive

If we are going to be honest about this comparison, we have to say clearly where Oregon is not the winner.

Oregon still has a high income tax. For high earners and retirees taking substantial distributions, that is real money.

And if we are talking specifically about Multnomah County, there are additional taxes layered on top.

- Preschool for All tax, which increased and now reaches 2.3% on incomes over $125,000 and 3.8% on incomes over $250,000

- Metro Supportive Housing Services tax, another 1% on income over $125,000

So no, Oregon is not the low-tax paradise in this comparison. Not if income is the only line item we care about.

But there has also been an important flip on the estate tax side.

Oregon used to be notorious for its low estate tax exemption. According to the information laid out here, as of 2026 Oregon raised its exemption to match the federal level, meaning most estates under roughly $15 million would pay nothing.

Washington, meanwhile, sits around a $3 million exemption and now has a top estate tax rate of 35% for larger estates.

That changes the conversation for families thinking not only about annual taxes but also about what they eventually leave behind.

The cleanest way to frame it is this:

- Oregon’s tax burden is high, but largely known and easier to model

- Washington’s tax burden is changing, and the direction has become less favorable for high earners, retirees, and possibly middle-income households over time

A Real-World Cost Comparison

Here is a practical scenario that mirrors a lot of households making this decision.

- Retired couple

- $200,000 annual income from IRA distributions and investment income

- $1 million home

- Two newer vehicles

- $80,000 in household spending per year, separate from housing costs

Using the numbers presented, the comparison looks something like this:

- State income tax today: Washington $0, Oregon about $17,000 to $19,000

- Sales tax on $80,000 spending: Washington about $8,200, Oregon $0

- Vehicle registration for two cars: Washington about $1,400 to $1,800, Oregon about $400

- REET on future $1 million home sale, spread over 15 years: Washington about $1,120 per year equivalent, Oregon $0

- Estate tax on a $5 million estate: Washington about $450,000 total, Oregon $0 under the framework described here

On annual cash flow alone, Washington still comes out ahead in this example, but only by roughly $5,000 per year after accounting for Oregon’s hidden advantages.

That is the key takeaway. Washington is not miles ahead anymore.

And if Washington eventually expands its income tax structure even modestly, that lead can disappear quickly. A simple 3% tax on $200,000 of income would be $6,000, enough to erase the current cash flow edge and tilt the math the other direction.

That is why trajectory matters.

Why Many People Still Choose Oregon

Of course, people do not move to the Portland area only for tax optimization.

They move because family is here. Because work is here. Because they want to be near kids, grandkids, schools, neighborhoods, and communities that fit the next chapter of life.

And that is where the Oregon side continues to make a strong case.

Lake Oswego offers a walkable downtown and a beautiful lake-centered community. The West Hills offer privacy, views, and a kind of natural beauty that is hard to replicate. The broader Portland area offers outstanding food, strong outdoor access, and a quality of life that many people find genuinely special.

That does not make Oregon perfect. It does mean that when the financial gap narrows, lifestyle starts to matter even more.

And for many households, that balance now favors Oregon more than it did a few years ago.

Final Thought

If we are retirees who were told years ago to buy in Clark County for tax reasons, it may be time to revisit the analysis.

If we are high earners relocating for work or family, especially with household income over $150,000, this is no longer a default decision. It deserves updated numbers.

If we already live in Washington and are wondering whether moving across the river still makes sense, the answer may be different now than it was when we first made that choice.

The real question is not just what we pay this year. It is where each state appears to be heading over the next 5, 10, and 15 years.

For a long time, Washington represented the straightforward tax play. Today, Oregon looks more like the state of stability, while Washington looks more like the state of tax uncertainty.

That does not make Oregon automatically better for everyone. It does mean the old assumptions deserve to be retired.

If you’re moving to the Portland metro —whether you’re weighing Portland vs. the Washington side of the river, relocating for work, or trying to protect retirement income—don’t rely on outdated “no income tax” rules of thumb.

Get help running the numbers for your situation(income, spending, vehicle costs, and your likely home price range). Schedule a buyer consultation here, and we’ll talk through the real cost differences so you can make a confident move.

Prefer to start early? Download our free relocation guide to map out neighborhoods, budgets, and next steps.

FAQ

Is Washington still cheaper than Oregon for retirees?

It can be, but the gap is much smaller than it used to be. Washington still has the advantage on state income tax today, but Oregon offsets a lot of that through no sales tax, lower vehicle-related costs, no statewide real estate excise tax, and potentially much better estate tax treatment under the numbers discussed here.

Why are more people reconsidering Vancouver, Washington?

Because the two biggest reasons people moved there, no state income tax and better housing value, are both less powerful than they used to be. Housing in parts of Clark County is no longer clearly cheaper than Portland, and Washington’s tax framework is changing.

What is the biggest financial advantage of living in Oregon?

For many households, it is Oregon’s lack of sales tax. That affects everything from everyday spending to car purchases. Depending on spending habits, that can quietly save thousands of dollars per year.

What is the biggest drawback of living in Oregon?

The biggest drawback is Oregon’s income tax, especially for high earners and retirees taking significant distributions. In Multnomah County, local taxes can make that burden even higher.

Does Washington have a real estate sales tax when selling a home?

Washington has a real estate excise tax, or REET, that applies when a property is sold. On higher-priced homes, this can amount to many thousands of dollars. Oregon does not have a comparable statewide tax of that kind.

Should we choose Oregon or Washington based only on taxes?

No. Taxes matter, but this is still a lifestyle decision. Family location, commute, neighborhood fit, community feel, and long-term goals all matter. The best choice is the one that works both financially and personally.

As always, this is a strong reminder to run the numbers with a CPA or qualified tax professional before making a move. The details matter, and they are personal.

READ MORE: Moving to Portland? Here’s What Most Realtors Won’t Tell You